United States: Through massive government spending, China was able to stave off the major recession affecting much of the world in 2008–2009 and support the global economy.

A repeat of the Chinese-led recovery appears less likely as the world is "dangerously close" to entering a global recession due to Russia's conflict in Ukraine and three years of the COVID-19 pandemic.

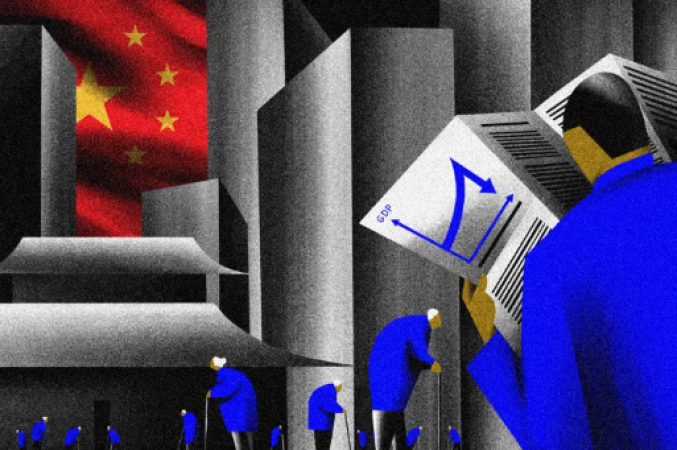

In 2022, the nation's economy grew only 3%. Growth is expected to remain sluggish in the first quarter of 2023 before picking up significantly in the second half of the year, according to a survey of 37 economists conducted by Nikkei in December.

Also Read: Russia-Ukraine war impact on the global economy

The group's predictions ranged widely between 4.0 and 5.9 percent, with the average GDP growth estimate coming in at 4.7 percent.

However, even the most upbeat recovery scenario for China does not portend a return to the explosive growth rates the nation had become accustomed to over the years. China's GDP has grown at an average of about 10 percent a year since Beijing began economic reforms in 1978.

In 2022, the nation's economy grew only 3%. Growth is expected to remain sluggish in the first quarter of 2023 before picking up significantly in the second half of the year, according to a survey of 37 economists conducted by Nikkei in December. The group's predictions ranged widely between 4.0 and 5.9 percent, with the average GDP growth estimate coming in at 4.7 percent.

However, even the most upbeat recovery scenario for China does not portend a return to the explosive growth rates the nation had become accustomed to over the years. Since Beijing began implementing economic reforms in 1978, China's GDP has grown by an average of about 10% annually.

The world's second largest economy has experienced many ups and downs since the pandemic first began. Repeated crackdown on the private sector and strict zero-Covid lockdowns have destabilized supply chains and eroded investor confidence after early optimism about the economy's recovery in 2020.

In additional bad news from January, last year the nation's population declined for the first time in 60 years, raising concerns about the future of the labor force.

Can China hope to return to sustained high growth now that President Xi Jinping has essentially cemented his position as the country's leader for the foreseeable future and the nation has finally moved out of zero-Covid ?

According to World Bank data, between the end of the century and 2021, China's economy grew rapidly over the long term from $1.2 trillion to nearly $18 trillion.

Also Read: 'PM Modi is one of the most powerful people on earth,' British MP praises fiercely

The GDP of the United States, which has the largest economy in the world, has slightly more than doubled since 2000.

However, according to predictions by economists Al Jazeera reported, China's growth rate will slow to between 2 and 5 percent in the coming years.

Even that, according to economist Michael Pettis, a senior fellow at the Beijing-based Carnegie Endowment for International Peace, hides a shift that has already happened.

Focusing only on GDP figures risks missing the bigger picture because they only provide a fragmented, delayed view of the Chinese economy.

According to statistics, the era of high growth seems to be coming to an end now, but in terms of productive investment, it ended about 10 to 15 years ago,

China's recent record-breaking growth was driven by exceptional demographic and economic conditions, but those conditions have since faded.

As China's population continues to grow rapidly, the large labor pool supporting its low-cost industrial base is getting smaller. In 2022, the country's population begins to decline after several years of slow birth rates.

This year, India will overtake China in terms of population as multinational corporations continue to move more manufacturing to countries in Asia such as Vietnam, Malaysia, India and Bangladesh.

Debt-fuelled infrastructure and real estate investment that has historically fueled China's growth has also hit its peak. According to Hung Tran, a senior fellow at the Atlantic Council, the returns on these investments are diminishing.

Total factor productivity, which measures how much the economy actually produces as a percentage of inputs, is no longer growing as fast in China as it used to be.

Before 2008, productivity growth averaged 2.8 percent, but since then it has declined to just 0.7 percent annually.

As evidenced by the collapse of the largest real estate developer in the nation, Evergrande, in 2021, this has left many heavily leveraged businesses and local governments on the verge of collapse.

There are definitely some levers China's leaders could use to lessen the discomfort of change. In order to "increase the labour participation rate of the economy - a measure successfully employed by Japan," they could raise the official retirement age for men and women, which is currently 60 and 55 respectively, to 65.

Even so, the crisis might only be partially postponed: After reaching a peak of just under 1 billion people in 2015, China's population in the 15- to 64-year-old age range is already declining.

Hung suggested that getting rid of the hukou system, which links social benefits to household registration, could boost urbanisation levels and support China's labour force.

The current system frequently denies state benefits like public education to migrant workers in cities, acting as a barrier to further urbanisation.

Building on China's sophisticated digital infrastructure to automate more manufacturing could also support maintaining industrial productivity.

However, Beijing's political leadership is establishing new priorities for China's journey even as it tries to calm an otherwise choppy descent into a lower growth altitude.

Beijing's policy priorities under Xi have shifted away from the mantra of "growth at all costs" that was followed by previous post-reform leaders. He has instead placed a focus on "high-quality growth," which is a guiding principle in China's current five-year plan.

It is a component of Xi's "new development concept," which places an emphasis on China's economic equality and resilience to external pressure.

In essence, experts said, the plan is to create a domestic consumption-driven economy to lessen China's reliance on export-driven growth.

A strong domestic market can serve as a shock absorber for sanctions from the West and a volatile international trading system. In addition to pursuing cutting-edge technologies like quantum computing and advanced semiconductors, China's new strategy aims to lessen the country's carbon footprint.

The need for domestic development of these technologies has increased as a result of a wave of stringent export control measures implemented by the US with the intention of destroying China's chip industry.

Though not equally, the slowing of China's growth engine will affect everyone.

Also Read: EU auto industry body reports a decline in sales

Many nations will feel the decline in demand keenly, especially those that have come to rely on China as their primary export market. The winners and losers during this transition will be largely determined by how quickly nations can switch to other faster-growing emerging markets, like those in Southeast Asia and India.

The geopolitical power balance will also be impacted by the slowdown. If China's economy reaches its peak in the next ten years, it will be less likely that it will overtake the US as the world's superpower.

Experts have cautioned that such a scenario could push Beijing to act more rashly on issues it sees as its "core interests," such as Taiwan's status, while it is at the height of its power