Planning your finances is crucial to ensuring a pleasant future. Annuity plans and fixed deposits are two well-liked financial vehicles that have drawn a lot of attention because of their stability and potential for rewards. These financial instruments make excellent pension plans in India and may play a key role in creating a solid retirement strategy.

What is an annuity plan?

An annuity plan is a contract between an individual and an insurance company. In this plan, the individual pays a lump sum amount or a series of payments in exchange for regular disbursements made by the company after retirement.

Features and benefits of annuity plans

● Guaranteed income

Annuity plans provide a stable stream of income after retirement, supporting one’s golden years.

● Flexibility

They have different payout options such as immediate annuity and deferred annuity.

● Life cover

Some annuity plans additionally offer a life cover benefit.

● Tax benefits

Annuity plans offer tax benefits as per Section 80CCC of the Income Tax Act.

● Protection against longevity risk

Annuities provide lifelong income, ensuring that the individual will not outlive their savings.

What is a fixed deposit?

The fixed deposit is an investment product where an individual deposits a lump sum amount with a bank or a financial institution for a predetermined period and earns interest over that period.

Features and benefits of fixed deposits

● Assured returns

Fixed deposits guarantee a fixed rate of return irrespective of market swings.

● Safety

They are often considered as one of the safest investment options.

● Flexibility

The fixed deposit provides a variety of tenure options, generally from 7 days to 10 years.

● Loan facility

Banks offer collateral loan against fixed deposits of up to 90% of the deposit amount.

● Tax benefits

Tax saver fixed deposits are deductible under Section 80C of the Income Tax Act.

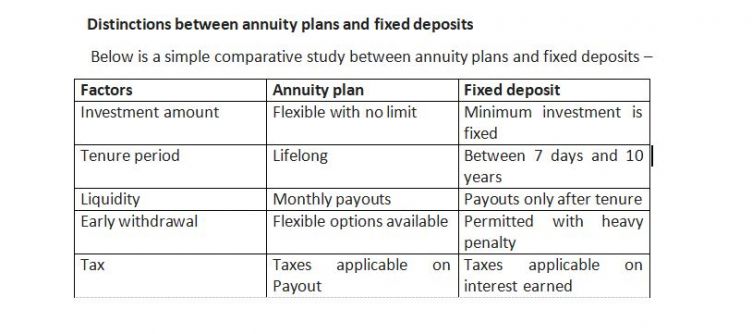

● Investment amount

Fixed deposits are highly flexible when it comes to the investment amount. With just Rs 1000, you can open a fixed deposit account which is a more affordable option for many. This flexibility endows individuals from different economic groups the opportunity to invest and grow their wealth over time.

However, annuity plans have a very large initial payment. This amount of lump sum is utilised by the company to generate and provide a guaranteed income for the retirement period. Even though the initial investment is high, the dividends in the form of stable retirement income can make it a profitable investment.

● Liquidity

Liquidity is the measure of how fast an investment can be converted into cash. Fixed deposits are highly liquid. While they are parked to be held until maturity, many banks permit premature withdrawal of deposits. But this comes with a penalty, which is adjusted against the offered interest rate.

Annuity plans may not be as liquid. After you invest in an annuity plan, the money is usually immobilised for a long time. This could be until retirement or for a fixed number of years, depending on the agreement. This lack of liquidity implies that you can't get your hands on these funds in the event of an emergency.

● Tenure period

The term of a fixed deposit can be extremely flexible. According to your financial objectives, you can select a tenure from seven days to ten years. This helps you to match your investment with your financial goals.

On the other hand, annuity plans are long-term investments. They are designed to be a regular source of income post-retirement. This is a long-term income that can secure your financial well-being and peace of mind through your retirement years.

● Early withdrawal

Fixed deposits provide for early withdrawal. If you need to access your funds before the maturity date, you can go ahead. Nevertheless, an early withdrawal penalty is levied. It could be in the form of a lower interest rate.

However, annuity arrangements do not allow for early withdrawals. An annuity's fund cannot normally be withdrawn until the end of the tenure. This might be a drawback if you suddenly need to access your money.

● Tax and risk on investment

Annuity plans and fixed deposits both have tax advantages. Under the Income Tax Act Section 80C, fixed deposits are eligible for tax deductions. Similarly, Section 80CCC allows contributions made to annuity schemes to be deductible.

However, each kind of investment has a different level of risk. As they provide guaranteed returns and are not dependent on the market, fixed deposits are considered a safer alternative. Although annuity plans do provide a steady income, they are riskier as the payment is subject to fluctuations in interest rates and other factors like inflation.

Your retirement plans, risk tolerance, and financial objectives, all play a major role in your decision to choose a fixed deposit or an annuity plan. With their special benefits and features, both make great pension plans in India. For this reason, it is wise to take into account both of these products in your financial planning in order to guarantee a stable and well-rounded retirement.

_676d0b9d3bd1a.jpg)